No More Growth? Let’s not be so Hasty: An Assessment of Robert J. Gordon’s Recent Working Paper

[caption id="attachment_4304" align="alignleft" width="594"] Source: http://thevaluesquad.com[/caption]

Source: http://thevaluesquad.com[/caption]

The single most important question regarding the future of the U.S. economy is whether productivity growth will be robust going forward. Recently there has been vigorous debate over this question, with some like MIT’s Erik Brynjolfsson arguing for robust, and others like George Mason’s Tyler Cowen arguing for stagnation. The newest foray into this debate comes from Northwestern’s noted economist Robert J. Gordon, through a non-peer-reviewed working paper published by the National Bureau of Economic Research (NBER) entitled "Is U.S. Economic Growth Over? Faltering Innovation Confronts the Six Headwinds." Gordon’s paper has received widespread attention for his provocative thesis that U.S. productivity growth is essentially over and that the average American will be no better off, and likely worse off in the future. No wonder neo-classical economics is called the dismal science. Luckily, innovation economics can be called “hopeful” science, for as I will explain; I believe Gordon’s thesis is fundamentally wrong.

Gordon’s paper is framed in two parts. First he argues that productivity growth (output per hour) in the recent past has been weak and will cascade towards zero and remain there for the foreseeable future. Second, he asserts that the U.S. economy will face six stiff “headwinds” that will lower productivity even further and lower median income. The primary reason that Gordon’s paper has received so much attention is that it offers a “provocative” departure from the existing economic research. However, provocative does not mean correct.

I see two fundamental problems with Gordon’s claims. First, Gordon does not appear to understand the information and communications technology (IT) system and its potential to drive productivity growth. In addition, because he is intent on making his case that IT has not driven productivity; he presents a distorted analysis of the growth data. Second, only one of Gordon’s six “headwinds” (education stagnation) has the potential to negatively impact productivity (which I argue it will not), while the other five affect either the overall size of economy or the distribution of the gains of productivity (e.g., growth in median real disposable income). To claim that future median income growth is likely to be stagnant is very different than saying that future innovation and productivity growth will be stagnant. Though the two can be related, they are very separate issues.

Part 1: Gordon’s Claim that the United States is Bound for Medieval Productivity Growth

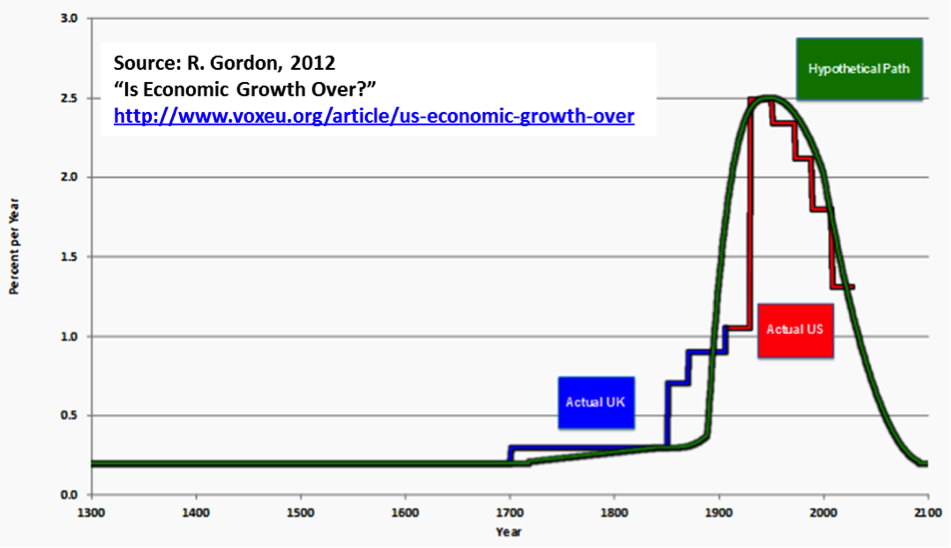

The first part of Gordon’s paper lays out his claim that productivity and GDP growth of a level above 0.2 percent per year has been an anomaly of the last 150 years. Gordon’s argument boils down to this: “The frontier established by the U.S. for output per capita, and the U. K. before it, gradually began to grow more rapidly after 1750, reached its fastest growth rate in the middle of the 20th century, and has slowed down since. It is in the process of slowing down further.” The core arguments and forecast of the paper are presented in the following graph. The validity of the data is crucial, as it is the basis of his “provocative forecast.” As such, let’s consider his data and its presentation.

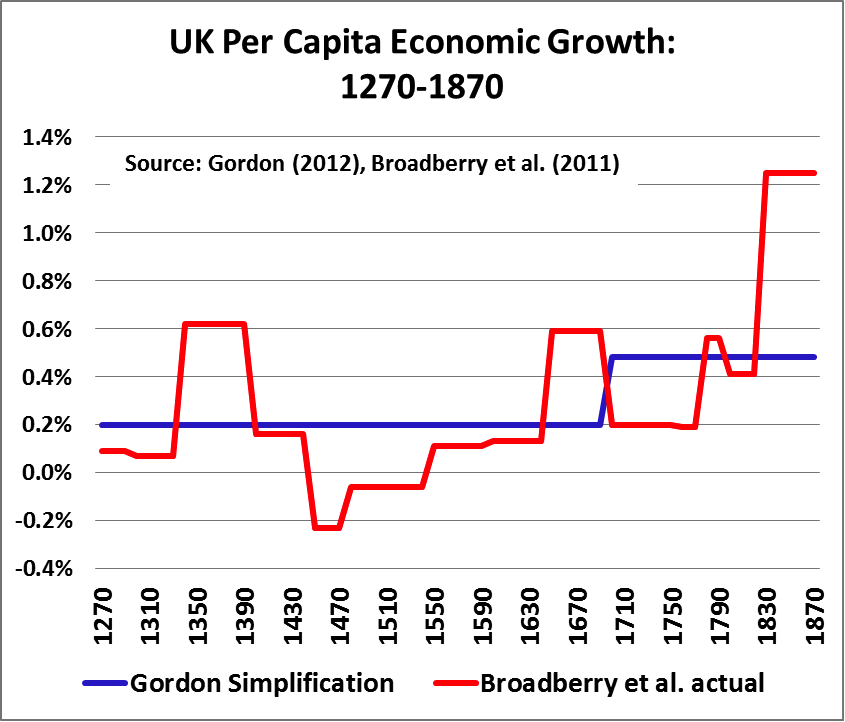

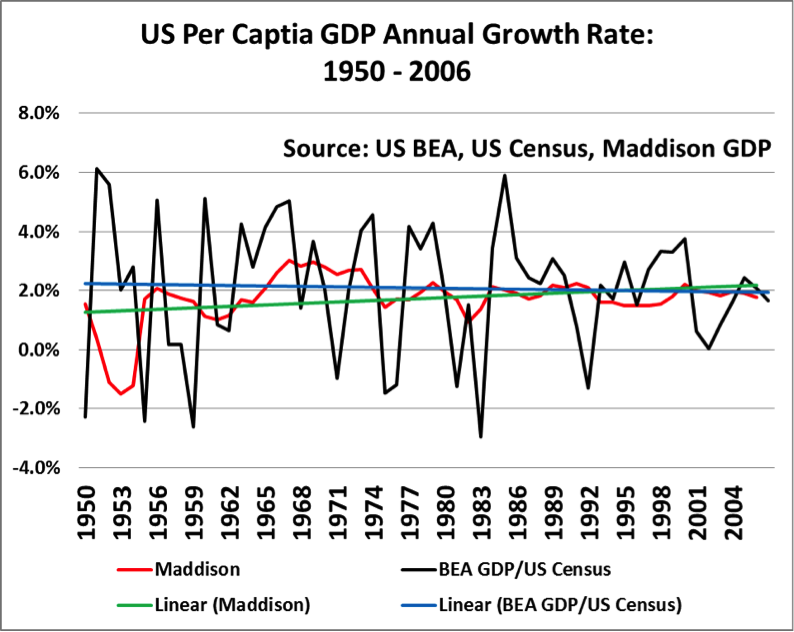

Gordon claims that growth was just above zero prior to 1700, that growth only rose after the first industrial revolution and that there has been a series of increasingly large declines since 1950. It is from this that Gordon claims we are headed back to the “natural” long run rate of economic growth: 0.2 percent. However Roger Pielke Jr. shows clearly in the two following graphs that not only was growth in the United Kingdom far from flat from 1270-1870 but that decline of productivity from 1950 does not follow the stair-step decline Gordon suggests.

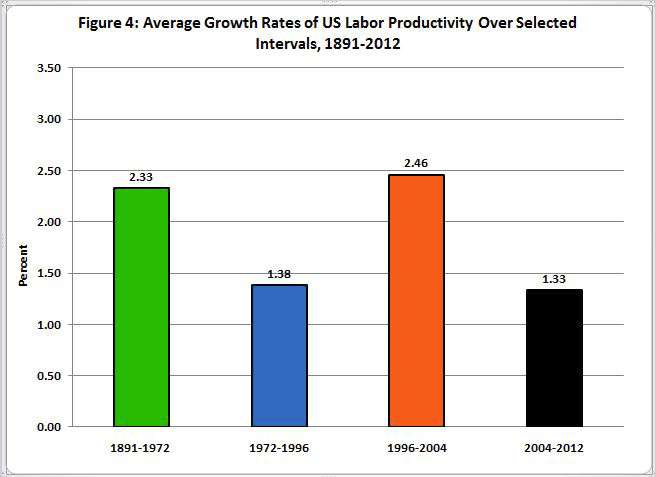

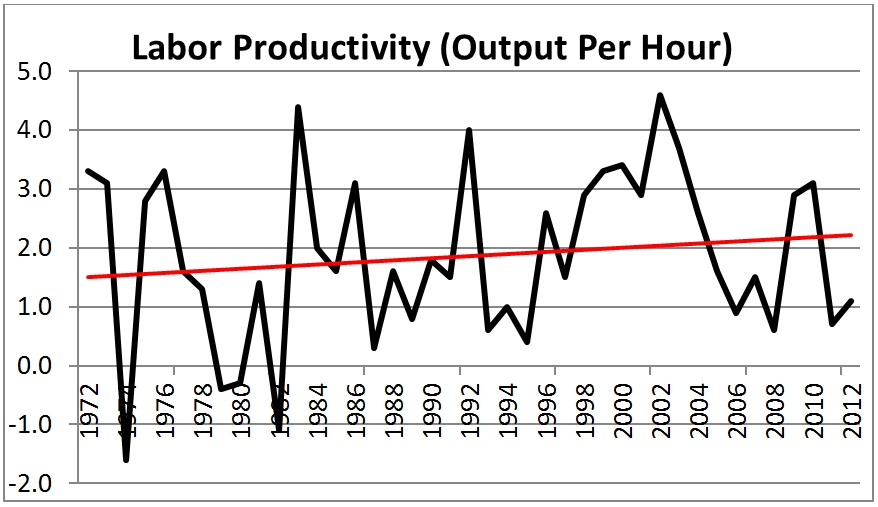

For Gordon to support his pessimistic argument he must find a way to explain away the very strong productivity growth experienced from 1996 through 2004. Gordon says that as of 2004, the gains related to IT were already realized and that today the growth engine is out of gas. He shows the following bar chart as proof of the collapse in productivity gains; stating that from 2004 to the present we have reverted back to pre-IT productivity levels, and that the declines from 1972 to 1996 will now continue.

For Gordon to support his pessimistic argument he must find a way to explain away the very strong productivity growth experienced from 1996 through 2004. Gordon says that as of 2004, the gains related to IT were already realized and that today the growth engine is out of gas. He shows the following bar chart as proof of the collapse in productivity gains; stating that from 2004 to the present we have reverted back to pre-IT productivity levels, and that the declines from 1972 to 1996 will now continue.

However, according to the following graph produced from the Bureau of Labor Statistics (BLS) productivity data; there is no systematic 40 year decline in productivity with a brief IT-blip. Rather, productivity is quite volatile with no remarkable pattern, except that it continues to trend upward. Moreover, if IT driven productivity is over, how is it that productivity in 2009 and 2010 exceeded 3 percent per year?

In short, by lumping data together in a subjective manner, one can always make it tell the story they want it to.

Aside from the apparent data concerns, let’s consider Gordon’s claim that the IT revolution has run its course. Gordon makes the mistake some other economist do: what we call the “only changes in form drive innovation” fallacy. This view essentially holds the only real innovations are ones we can see and touch: tall buildings, fast cars, indoor plumbing. But this misses the fundamental point that today’s innovations are not based on changes in form (e.g., physical discoveries like steel bridges and cars) but in function (digital systems that allow for the existing economic activities to be conducted much more productively). In other words, it is very likely that the world of 50 years in America will look pretty much like the world of today, not like the world of the Star Trek – cars will still drive the streets, buildings will be similar, we will be wearing the same kind of clothes. But the world of 50 years from now will operate much differently (and more productively.) The IT revolution isn’t over; it’s in its infancy.

Gordon’s misunderstanding of how technology affects productivity is evident in is his discussion of past innovations. As an example of one-time innovations (change in form), Gordon claims that there is “no better illustration than transport speed. Until 1830 the speed of passenger and freight traffic was limited by that of “the hoof and the sail” and increased steadily until the introduction of the Boeing 707 in 1958. Since then there has been no change in speed at all and in fact airplanes fly slower now than in 1958 because of the need to conserve fuel.” However, this illustration misses two things. First, productivity of air travel is not only a function of speed (the final product); it’s a function of price (the process used to produce the final product). In fact, aviation productivity has grown 2 percent per year on average from 1973 through 2001 which is one reason why air travel is so affordable. Second, Gordon fails to recognize that there are still immense productivity gains to be had in aviation. We probably won’t get supersonic ramjets but the way the entire system works will be dramatically changed from the inside out, through the incorporation of IT-innovations. In fact, already on the drawing board are systems to allow people to check into flights without ever stopping to do so. In addition, with the GPS-based NextGen that the FAA is working on, planes may not travel faster, but there will fewer delays, more direct “as the crow flies” flights, and more flexibility to get around weather problems.

Certainly, significant IT-driven productivity gains won’t be isolated within air travel, but in surface transportation as well. Just consider one of the examples that Gordon himself mentions: Google’s prototype self-driving car. Commercial and passenger vehicles will be more time and energy efficient while also reducing accidents (all productivity gains). Consider a plausible scenario where the use of a smart-grid and smart-self-driving-cars reduced urban commute times by 30 percent. According to a poll conducted in 2005, the average U.S. citizen spends 9,100 hours commuting to/from work. So, this increase in productivity is equivalent to increasing the average worker’s output by 68 weeks of work, or over a year and a half in the average 40 hour-per-week job. This change alone has the potential to increase total output in the economy by 3.3 percent. (1.5 years divided by 45 years, the number of years in the labor force.) That’s not to say that all time save through lowered commute times would all go towards working, certainly productivity gains can be enjoyed by increasing leisure time; but this gives a glimpse as to the size of economic waste that is still being generated on a daily basis.

The opportunities to reduce wasted time and resources throughout the economy through the incorporation of IT are innumerable. As a final illustration, the self-service and transaction-based economy has been completely transformed through innovation and adaptation of IT (self-check-out, online banking, online realty, online travel booking etc.) As a result, these low productivity jobs have shrunk, making way for new utilization of that labor in more highly productive non-routine jobs. This is similar to the trend of the early 1900s when the number of farmers shrank when the tractor was adopted as Gordon explains (which was a “basic” source of very rapid growth). In short, the IT revolution has only just begun. As IT innovation proliferates and is adapted, every part of our daily lives will be transformed at the process level, not the output level.

Assessing Part 2: The Six Headwinds

The second part of Gordon’s paper is quite separate from his initial argument that growth tends towards zero. He proposes that the United States faces six headwinds to growth. However, despite what Gordon implies, only one of these “headwinds” has the potential to negatively affect productivity, and that is education.

Gordon claims that educational achievement has plateaued as measured by the number of years of education attained and that affordability has limited the ability of those with lower income to attain a college degree. Therefore, increases in education can no longer contribute to productivity growth. But if we could reduce the high school dropout in half from its current xx percent, we would significantly increase educational achievement. In addition, as massive open online course (MOOCs) and other IT-driven educational opportunities proliferate, education l costs fall and thereby expand educational opportunities for those that Gordon claims can’t afford higher education any longer.

But more importantly as Hanushek shows it isn’t the number of years of education that matter for growth and innovation, rather the quality of education. And on that score the United States has a very long way to go in order to reach its potential. Strikingly, among U.S. college seniors, just 34, 38 and 40 percent were proficient in prose, document, and quantitative literacy, respectively. Clearly, significant opportunities exist by which the current educational system can be made more effective and productive.

Gordon’s remaining five headwinds simply do not negatively impact productivity growth; rather they are associated with the overall level of GDP or the income distribution, which is quite different.

Globalization:

Gordon argues is that increased globalization will result in stagnant U.S. wages. To be clear, lower wages in other nations can result in a change in income distribution in the United States. Occupations that are more exposed to competition from low wage nations (e.g., jobs in textile factories) will see slower relative wage growth (or even decline) than occupations not exposed to low wage competition. But this has no effect on overall wages (e.g. the size of GDP) because low wage imports mean lower prices to American consumers. The reality is that wage rates in other nations have no effect on overall real wages in the United States. What determines real wages is U.S. productivity. Wages are simply a mechanism an economy uses to distribute economic output. The only way that trade can lower U.S. wages is if it shifts the composition of output to be of lower productivity. It is true that this has happened in some sectors, but it is certainly not inevitable as has been seen in the advanced manufacturing industry. With the right policies, including trade agreements that work to limit foreign innovation mercantilism, as explained in “Enough is Enough: Confronting Chinese Innovation Mercantilism,” high wage jobs in traded industries could in fact grow.

Income Inequality:

Gordon claims that increased income inequality is a major headwind. Relying on data by Emanuel Saez and Thomas Piketty he shows that those at the bottom of the earnings distribution have fared less well than those at the top. But as ITIF’s report by Stephen Rose has shown, Saez and Piketty overstate the growth of inequality. Moreover, Gordon does not explain how increased inequality inhibits future growth, and there is a reason. Saez and Piketty, in fact do not support his inference. They say clearly that “causal examination…suggests income concentration and growth are not systematically related.” Daron Acemoglu and James Robinson in their new book “Why Nations Fail,” argue that it is clearly institutional design and education that dually set the stage for growth and inequality. Inequality and redistribution are questions of fairness, but do not appear to be determinants of productivity.

Demographics:

Gordon rightly notes that an aging population will mean slower GDP growth because a smaller share of people will be working. But this is quite different from lower productivity, and has virtually nothing to do with innovative capacity. Working less hours in does not result in lower productivity growth, it just decreases total output. Productivity is output per hour of work. In fact, productivity is the key to solving this baby-boomer problem. Only by producing more with less will the smaller workforce be able to produce enough to provide for the larger proportion of the population that is not self-sufficient. Again, this does not hinder productivity and innovation, if anything it spurs it, if for no other reason that it becomes clearer to policy makers that they need to put in place a national productivity agenda.

Climate Change and Carbon Taxes:

Gordon says that increased taxes on pollution and increased concern with energy will lead to lower growth. Gordon uses China as an example of the growth that is possible if environmental regulations were reduced in the United States. However, the short-run growth that China has enjoyed has little to do with lax environment regulations. In fact, in its latest release the World Bank states that the primary policy concern in China is to steer the Chinese economy towards a more sustainable growth path. Likewise, he argues that actions to reduce global warming in the United States will cost money and therefore slow growth. As has been clearly shown by Stepp and Atkinson in “An Innovation Carbon Price: Spurring Clean Energy Innovation While Advancing U.S. Competitiveness,” the reality is that clean energy innovation could lead to lower cost energy which would increase growth. In addition, by reducing pollution and managing the extraction of natural resources at a sustainable rate, the United States could ensure that long-run growth is possible.

Deficits and Debt:

The last headwind is the U.S. deficit and debt problem. Gordon says that the large recent increases in debt will inhibit future growth. But this is a consumption issue, not a growth or productivity issue. High debt or spending deficits do not necessarily affect the potential of future innovation. Rather, the solution to public deficits and debt will affect personal after-tax consumption levels, because there will need to be relatively less public spending and relatively higher taxes. However, this does not mean that productivity growth will fall. In fact, as constraints become more binding, it spurs the private sector to reduce costs through; bolstering innovation rather than hindering it.

Conclusion:

If Gordon were writing a paper on the future of the median U.S. consumer, then more of his paper would be relevant. However, he titled it as “Is U.S. Economic Growth Over? Faltering Innovation Confronts The Six Headwinds.” Because of the misunderstanding of IT’s productivity potential, irreconcilable data, and faulty linkages between the headwinds and innovation, this paper should not be regarded as providing an accurate explanation of where the U.S. is headed over the next 50 years.

This is not to say that the U.S. economy does not face significant problems stemming from the great recession. However, there are clear solutions to our “growth problems.” We need a national innovation and productivity policy that is instituted on an industry by industry basis; determining what the productivity opportunities and barriers are in major industries and then instituting clear policies to spur higher productivity. We also need better “inputs” to productivity and innovation, including higher quality education and more support for research and development. The tax code could do a better job of spurring innovation and productivity, especially by having a permanent and expanded R&D tax credit and an investment tax credit. Even so, the future is not nearly as grim as Gordon would propose.

In Robert D. Atkinson’s book “The Past and Future of America’s Economy: Long Waves of Innovation that Power Cycles of Growth” this incite by Harvard Kennedy School’s F.M. Scherer is noted:

“There is a centuries’ old tradition of gazing with wonder at recent technological achievements, surveying the difficulties that seem to thwart further improvements, and concluding that the most important inventions have been made and that it will be much more difficult to achieve comparable rates of advance. Such views have always been wrong in the past, and there is no reason to believe that they will be any more valid in the foreseeable future.”

Gordon’s pessimism is no different. Noted “hopeful” economist Joseph Schumpeter got it right more than half a century ago when he stated, “There is no reason to expect slackening of the rate of output through exhaustion of technological possibilities.” For Schumpeter, “Technological possibilities are an uncharted sea.” It is up to businesses, other organizations and policymakers to make the right decisions to make sure that we continue to sail into uncharted waters in that great sea of the unknown.